Performative White-Collar Executions Part 1: Build Your Bunker

The Icono Field Guide on how to survive Mark Zuckerberg's robot apocalypse

Hey Iconoclasts,

Something at the front of my mind lately has been the amount of clients we have been talking through layoffs through the lens of their financial plan.

The best time to prepare for a layoff is when your performance review is full of words like 'trajectory' and 'high-potential

I was still in college in 2008, and while the current environment feels nowhere close to that, this is the first time in my fifteen years in the business that layoffs feel like a trend rather than an event.

We have worked with 7 families through layoffs in 2026 and they are mostly higher earners like engineers, PMs, designers, and ad-sales people.

However, the most disturbing part is this new genre of laying people off. Call it what it is: the performative white-collar execution.

Layoffs as content. Termination as personal branding for leadership so the CEO can beg the audience to clap for his fucking vulnerability.

I think it’s one of the ugliest things happening in American business right now, and it’s been so normalized we’ve stopped noticing how bizarre it is. Forty years ago, executives doing layoffs at least had the decency to look ashamed. Now they’re posting about it like a personal growth arc.

Spoiler: the machine has slowed down. Actually, the machine is starting to make a weird grinding noise, and the guy who owns the machine is, as previously discussed, doing a brand-new mindfulness plunge cooldown routine on his social media.

The question is always some version of: how worried should I be, and what should I actually do if this happens to me?

So I put together a playbook for what I feel are the 3 phases of the current layoff environment.

Today’s Post: How to build your bunker while the paychecks are still hitting

Next Week’s: How to embrace your self-awareness and read the writing on the wall.

Part 3 Soon After: You’re already fucked. What now?

Phase 1: Build the Bunker

This phase requires you to take action while everything is fine, which can feel like the financial-planning equivalent of buying flood insurance in Phoenix.

The best time to prepare for a layoff is when your performance review is full of words like “trajectory” and “high-potential.” Because by the time those words become “headwinds” and “right-sizing,” you’re already down 30 with five minutes left and the coach is pulling the starters.

.jpg")

How big should your cash reserve actually be?

The 3-6 month1 emergency fund rule can be misleading. That math came from an economy where people found new jobs in eight weeks because there were fewer of them, less AI, and a corporate desperation to hire normal people.

Also, it shouldn’t be a catch-all - everyone’s life is different and their needs should adjust accordingly.

Here are variables we consider when recommending emergency fund amounts.

Baseline

Start with 6 months then +- months based on your situation.

Core adjustments

Children: +1 month each

Occupational volatility: + 1-3 months (commission, equity, or contract pay)

Health Concerns or expensive prescriptions: +1-3 months

Spouse/partner’s income: -1 to -3 months (zero discount if you’re both in the same industry)

Housing

Mortgage, as % of monthly expenses2

25-40% = +1 month

over 40% = +2-3 months

Rent, as % of monthly expenses

25-40% = +0-1 month

Over 40% = +1-2 months

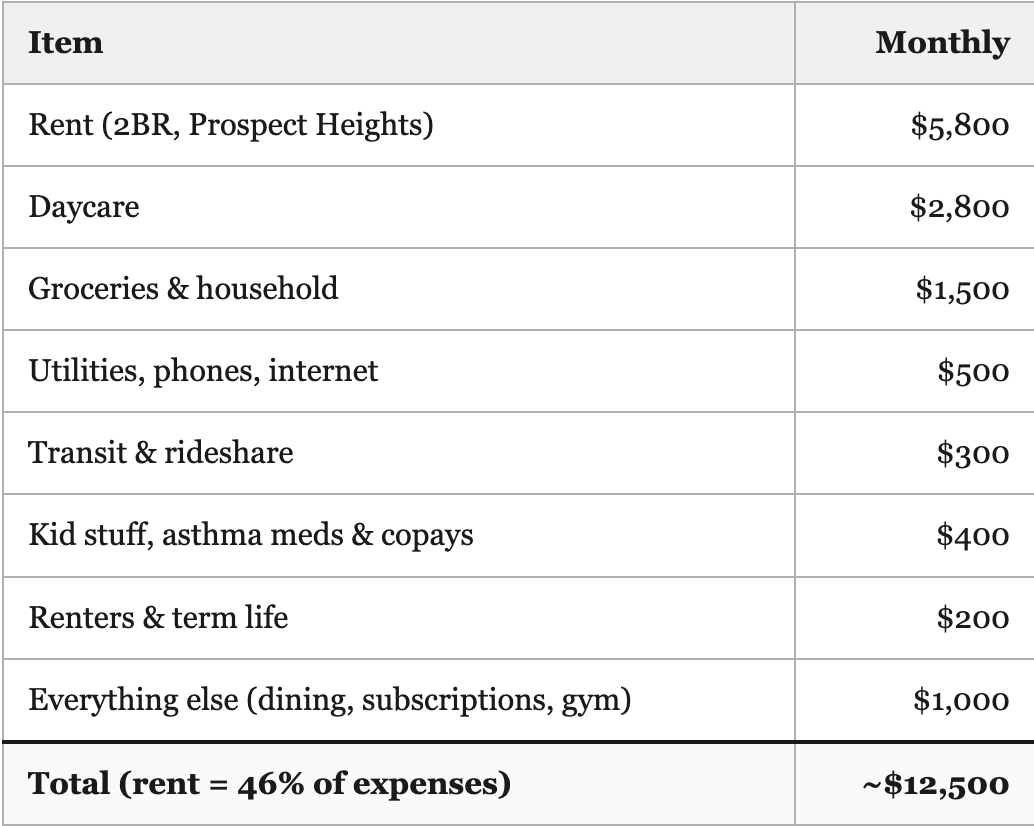

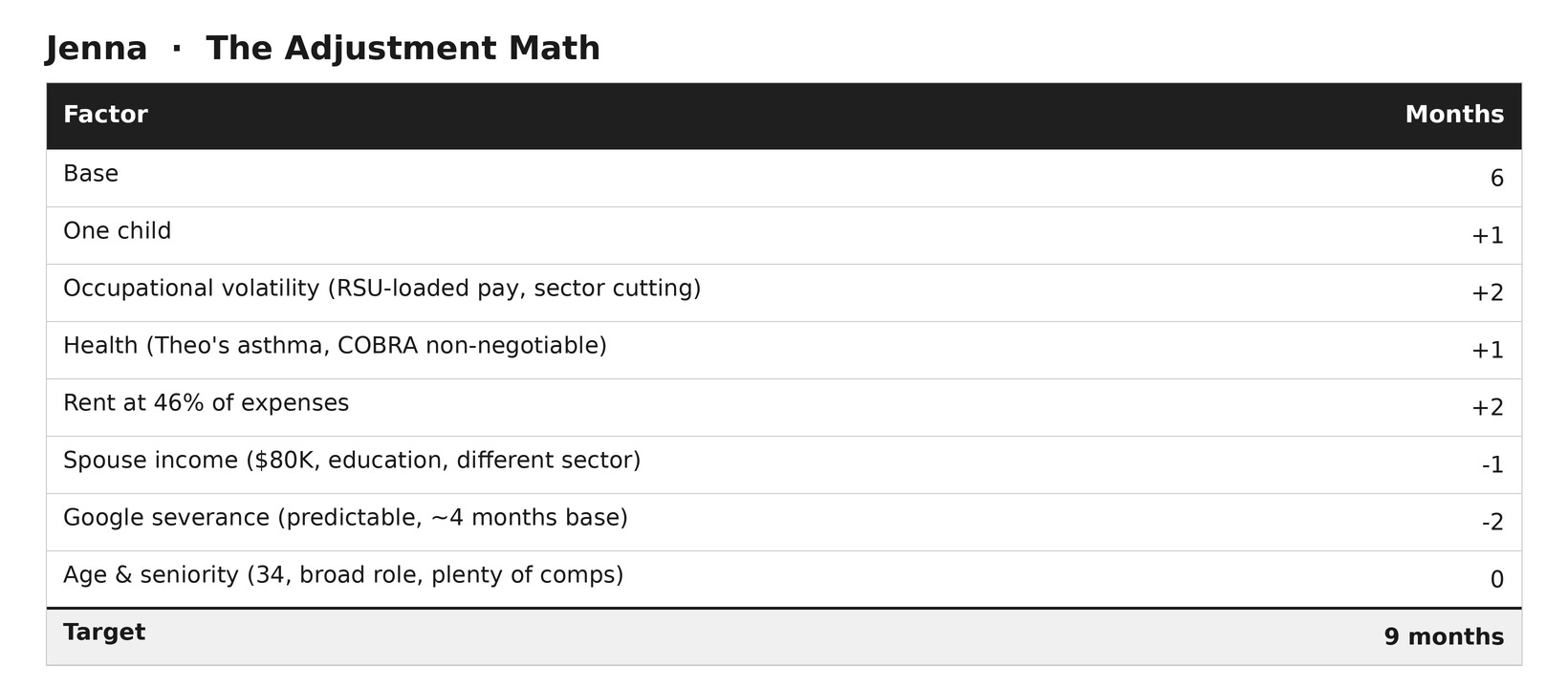

The math on a real Brooklyn household

Meet “Jenna”. She’s 34, an L5 software engineer at Google making about $400K all-in (base plus a stack of RSUs). Her husband “Mike”, 35, teaches at a charter school and pulls $80K. One kid, “Theo:, age 2, who has asthma (maintenance inhaler, a pulmonologist twice a year).

They rent a 2-bedroom in Prospect Heights for $5,800 a month and have no plans to leave Brooklyn before Theo starts kindergarten.

So, Jenna and Mike need to have $135,000 in an established emergency fund in this example.

Park this money in a high-yield savings account paying 3.5% APY3. NOT in your brokerage sweep or checking account, which is earning you roughly a quarter of a percent.

Stop letting your employer be your only bank.

Your paycheck, your RSUs, your ESPP, your 401(k) match, and probably your equity-heavy brokerage account are all denominated in the same currency: your employer’s continued affection for you.

When the layoff hits, it hits all of those at once. The stock drops (because the layoff signals weakness), your unvested RSUs evaporate into the ether (those were a promise, not an asset, and the promise is now void), your ESPP loses its discount, your 401(k) match stops, and you’re trying to job hunt while watching your net worth get its teeth kicked in over the course of a single calendar quarter.

Concentrated single-stock exposure above 15-20% of your liquid net worth is a leveraged bet on your continued employment. Diversify before you need to.

The actual tools for doing this realistically include:

Just effing sell when they vest! Set a reminder and do it.

10b5-1 plans4 (a preset selling schedule that pre-empts insider-trading concerns)

Exchange funds (swap your concentrated stock into a diversified pool without triggering the gain) like Cache5

Direct indexing with tax-loss harvesting

Everything you own is denominated in the same currency: your employer's continued affection for you.

This is a long conversation. We have it with clients constantly and it takes a while to build the full strategy, so don’t be discouraged.

Map your benefits like you’re planning a bank job

Sit down with your benefits portal one weekend, pour yourself something brown, and actually understand the following:

When do your next RSU tranches vest? If layoffs are rumored, this is the single most important piece of information in your entire financial life.

What does COBRA actually cost? Get a real quote. The number is going to make you laugh, then cry.

Check for a Mega Backdoor Roth (the after-tax 401(k) contribution that converts to Roth). This is the single best retirement tool most people don’t know they have

Do you have access to one, and have you been using it?

If layoffs are looming, max it before the badge goes dark. That window closes the second you’re out.

HSA balance: have you actually been investing those dollars, or letting them sit in the cash sweep earning enough to maybe buy an Uncrustable?

What does severance look like at your tenure level? Glassdoor, Levels.fyi, Blind. Real data is out there, so use it for your benefit.

Take the medical stuff seriously

While you have your good, cheap employer health insurance, use the hell out of it. Every doctor’s appointment you’ve been putting off. Every dental procedure your hygienist has been hinting about. New glasses, backup glasses. Refill every prescription to the max.

If you’ve been thinking about therapy, start now. Finding a new therapist while unemployed and stressed and trying to figure out whether your COBRA covers them is its own special hell, and the wait times in major cities are bordering on absurd.

COBRA can run you $2-3K a month for a family. Every uncovered medical thing you push into the post-layoff window is money straight out of the bunker.

The number of phone calls I’ve made to insurance companies in the last few months would make a 1970s switchboard operator weep.

The Bigger Picture

Forty years ago, executives doing layoffs at least had the decency to look ashamed. Now they’re posting about it like a personal growth arc.

For about fifteen years (roughly 2010 to 2025) there was an implicit handshake inside the new economy. You worked hard, you delivered, maybe you even got equity, the equity went up because the sector was in the middle of one of the great asset bubbles of human history, and the company “took care of you.”

The trade was loyalty for opportunity, and both sides held up their end mostly because the music never stopped.

The music is stopping babe, so build your bunker. Take care of your own goddamn self. Nobody is coming to save you. And you don’t need them to.

Part 2 next week: how to read the writing on the wall

Monthly expenses, not income.

You can’t shrink a mortgage in a hurry, and selling in a down market is its own trap.

As of 5/30/2026. Our Custodian Altruist pays 3.5% on their high yield cash accounts.

https://www.morganstanley.com/atwork/employees/learning-center/articles/understanding-10b5-1-trading-plans

https://usecache.com/companion/exchange-fund-tax-benefit-calculator